German pig market in June: Farmers in shock, hope rises for China

30-Jun-2026 (21 days ago)

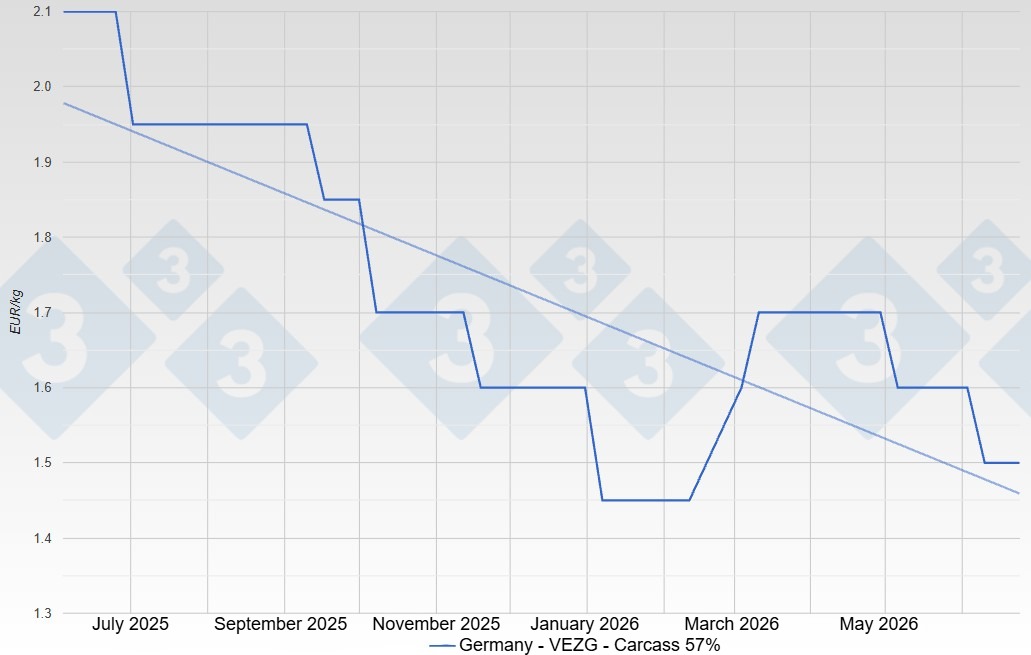

As the barbecue season got underway, expectations for stronger meat demand were high. Warm weather and several public holidays did provide temporary support for sales of grilling products, but the boost proved too weak to generate a sustained market recovery. Instead, the pork market remained well supplied throughout the month. At the same time, the public holidays reduced the number of slaughter days, leading to regional backlogs of market ready pigs and slowing down marketing activities. Slaughter companies pointed to difficult conditions in the meat market and increased pressure on producer prices. The German pig price initially held at €1.60, despite growing calls for price reductions. As the month progressed, however, market conditions deteriorated significantly and the price eventually dropped to €1.50. For many pig farmers, this came as a severe disappointment, as such a price decline during the peak barbecue season is highly unusual and further intensified the already difficult economic situation on farms.

Price pressure comes from demand, not supply

What made the situation particularly remarkable was that the weak price development was not caused by an oversupply of slaughter pigs. Pig numbers remained broadly in line with the previous year and therefore continued to be historically low. Following the substantial herd reductions of recent years, German pig production has settled at a much lower level. Slaughter weights also remained largely stable throughout June. The real weakness came from the demand side. While retail sales remained relatively steady, demand from the food service sector fell short of expectations. At the same time, many pork cuts could only be marketed through price concessions. Even traditional barbecue products failed to provide the seasonal momentum the industry had been hoping for. As a result, the meat market came under increasing pressure, and several slaughter companies reduced slaughter activities and processing capacity.

Piglets and cull sows also under pressure

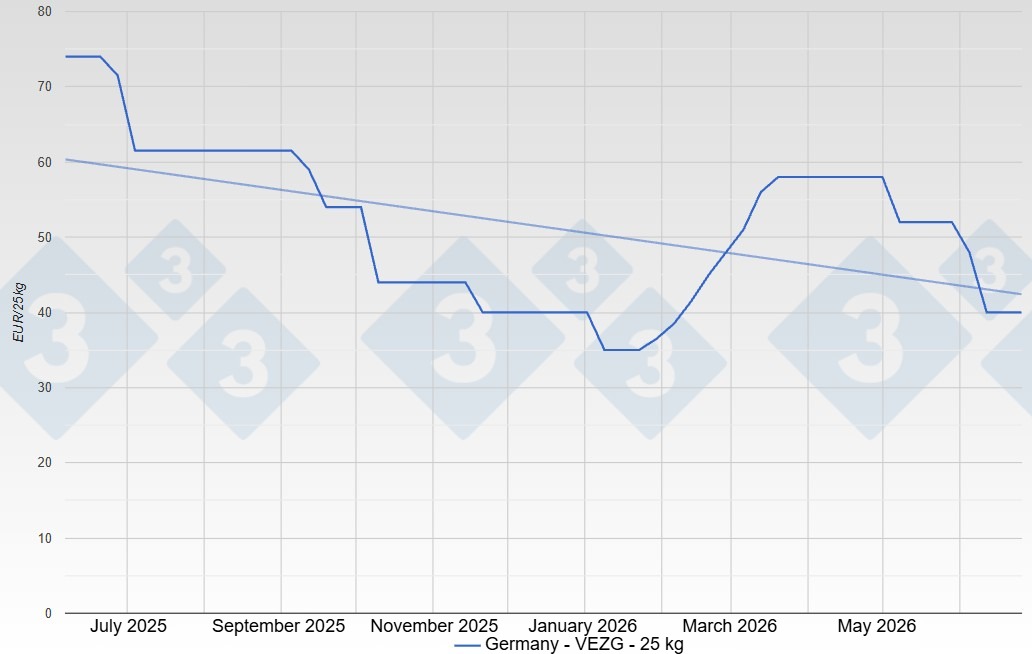

Conditions also deteriorated significantly on the piglet market during the month. Falling returns in pig finishing reduced farmers' willingness to restock, while free piglet batches became increasingly difficult to market. Price developments reflected this weak demand. After initially falling to €48.00, the German piglet price declined further to just €40.00 by the end of the month. This placed considerable pressure on piglet producers and increased the financial strain across the entire production chain.

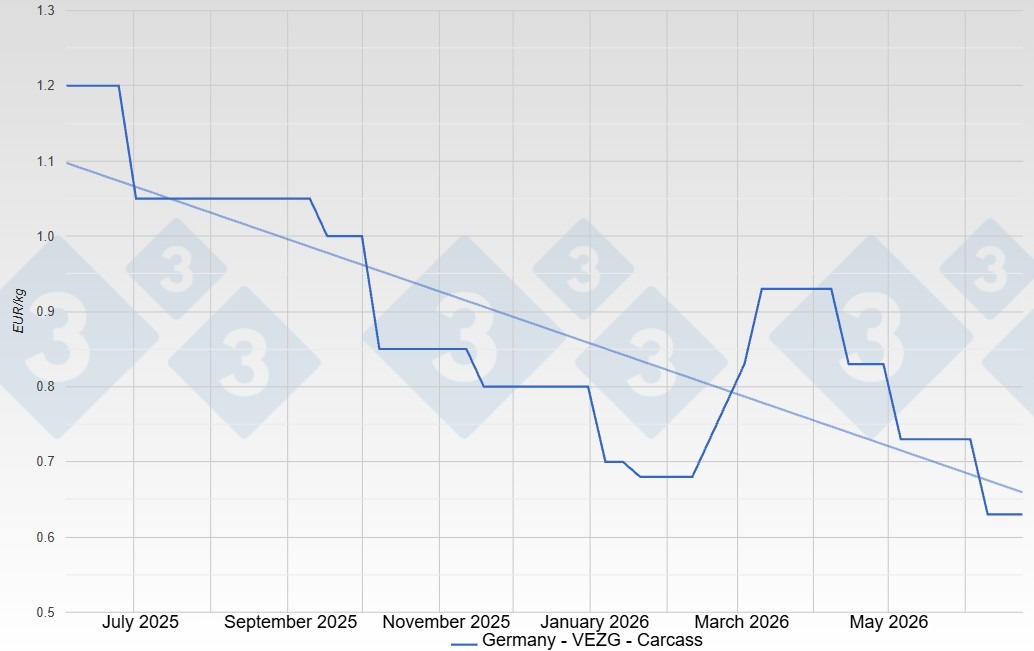

The cull sow market also showed little sign of recovery. Demand from the processing industry remained weak while supplies of sow meat were sufficient. At the same time, competitively priced offers from other European countries increased pressure on the German market. Marketing opportunities remained limited and few market participants expected any meaningful improvement in the short term. The difficult situation became particularly evident when Tönnies reduced its purchase prices for cull sows and simultaneously announced lower slaughter and cutting volumes. Other processors also adjusted their capacities to the sluggish market environment. Overall, the sow market remained under considerable pressure throughout June.

Policy adjustments and export hopes

Besides market developments, several political and structural issues gained importance during the month. Germany's “Initiative Tierwohl” introduced a few measures to simplify the transition towards its future full traceability system. At the same time, the organisation reaffirmed its long-term objective of ensuring complete traceability throughout the production chain. Transitional arrangements were introduced for sow and piglet producers to allow them more time to adapt to the new requirements. Farms will also be given greater flexibility to operate different production programmes at the same location. These measures are intended to improve planning certainty and facilitate continued participation in the animal welfare scheme.

At the same time, discussions intensified over how economic burdens should be distributed more fairly across the value chain. Many producers criticised the fact that, despite limited pig supplies, downward price pressure continued to intensify because the main challenges originated from weak meat demand rather than from excessive production.

Internationally, market conditions also remained uncertain. While Spain managed to perform somewhat better thanks to seasonally declining pig supplies and improved export opportunities, many other European pig markets continued to struggle. Belgium was forced to lower its pig prices again and market sentiment in the Netherlands also remained subdued.

At the same time, the industry's attention increasingly focused on new export opportunities. In particular, hopes were pinned on German Agriculture Minister Alois Rainer's visit to China, where discussions centred on negotiating a regionalisation agreement for pork exports. Such an agreement would be of major importance for Germany. In the event of a localised outbreak of African Swine Fever, exports would no longer have to be suspended from the entire country. Instead, only the affected regions would face trade restrictions. For the German pork sector, this would represent a major step towards regaining access to the Chinese market while reducing its strong dependence on the European internal market. Expectations were therefore high throughout June that the negotiations could produce meaningful progress.

Within Germany, discussions also intensified over how domestic pork could receive stronger market support. While retailers increasingly promote pork of German origin, such transparency is often lacking in wholesale trade and parts of the food service sector. From the industry's perspective, a stronger commitment to German pork would send an important signal to domestic producers and could help improve market conditions.

Cautious outlook despite limited pig supplies

Looking ahead, the outlook remains cautious. The still limited supply of slaughter pigs should, in principle, provide support to the market. However, any meaningful recovery will depend on stronger domestic consumption and improved export opportunities. Particular hopes remain linked to reopening the Chinese market, as additional export outlets outside Europe would significantly ease pressure on the European market.

At the same time, the remainder of the barbecue season and a possible recovery in food service demand will play an important role in determining market developments. As long as the European pork market remains well supplied and international competition stays intense, a sustained recovery is likely to remain gradual. June clearly demonstrated that even the peak barbecue season was unable to offset the structural weaknesses on the demand side. Only a simultaneous improvement in domestic demand and export opportunities is likely to create the conditions for a lasting recovery of the German pig market.